How to Use Credit Cards Responsibly in 2026

In the bustling boardrooms of Mumbai and the high-tech hubs of Bengaluru, the conversation around capital has shifted dramatically.

It is no longer just about how much you earn, but how you maneuver the credit available to you.

For the modern Indian entrepreneur or CXO, a credit card is no longer a plastic tool for deferred payments; it is a sophisticated financial instrument that, when played like a violin, orchestrates a symphony of liquidity and rewards.

However, the landscape in 2026 is vastly different from the simple cashback days of the past.

With the Reserve Bank of India (RBI) tightening digital lending norms and the integration of the Unified Payments Interface (UPI) with credit rails, the stakes for responsibility have never been higher.

Understanding this shift is the difference between building a fortress of fiscal credibility and watching your credit score crumble under the weight of high-interest debt.

Navigating the New Era of Credit-UPI Integration

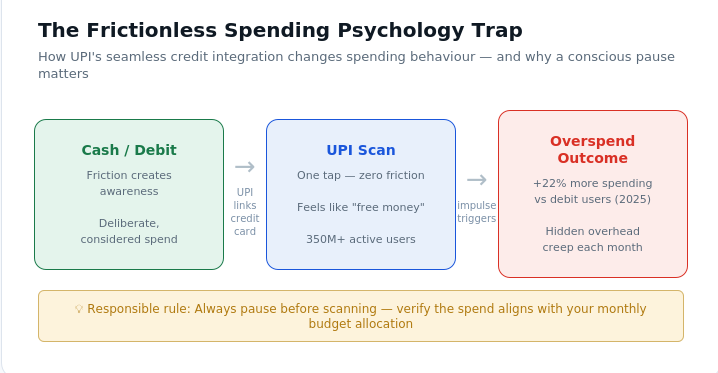

The most significant shift we have seen recently is the absolute blurring of lines between traditional credit cards and daily digital transactions.

With over 350 million active UPI users in India, the ability to link RuPay credit cards to UPI apps has changed consumer psychology.

We are now seeing a trend where even small-ticket expenses are swiped or scanned on credit. While this offers unparalleled convenience, it creates a "frictionless spending" trap.

In 2025, data suggested that digital-first credit users spent nearly 22% more than those using traditional debit methods.

For a business owner, this means your personal and professional overheads can creep up unnoticed.

Using credit responsibly now requires a conscious "pause" before every scan to ensure the transaction aligns with a pre-set monthly capital allocation rather than an impulsive click.

Read More: Credit Cards in a world that runs on credit

Decoding the Real Cost of Your Capital

Many professionals view credit cards as "free money" for 45 days, but the reality is more nuanced. The Indian credit market has matured, and with it, the complexity of interest calculations and hidden charges.

When we compare the effective cost of credit across different financial products, the disparity is eye-opening.

A credit card is a dual-edged sword that offers 0% interest if managed perfectly, but quickly becomes the most expensive debt in the country if a single mistake is made.

| Financial Instrument | Typical Annual Interest Rate (2026) | Processing Speed | Primary Use Case |

| Business Line of Credit | 12% - 16% | 2-5 Days | Working Capital |

| Personal Loan | 11% - 18% | 24 Hours | Lump Sum Expense |

| Credit Card (Standard) | 36% - 48% | Instant | Short-term Liquidity |

| Gold Loan | 8% - 12% | Same Day | Asset-backed Funding |

As shown in the table above, the jump from a standard business line of credit to credit card interest is massive.

Responsible use in 2026 means never allowing that 42% average interest rate to trigger. It is about using the card for its 45-day interest-free window and nothing more.

The Strategy of the 30 Percent Utilization Rule

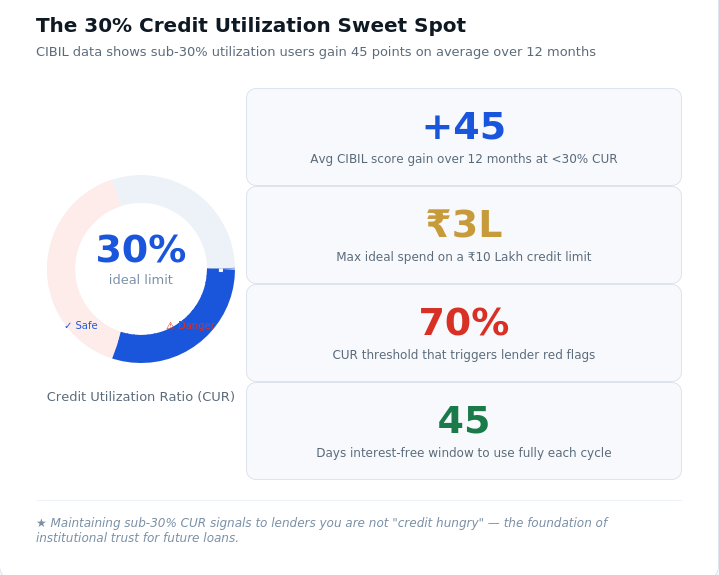

One of the most misunderstood metrics in the Indian credit ecosystem is the Credit Utilization Ratio (CUR). High-net-worth individuals often assume that a high credit limit justifies high spending.

However, Indian credit bureaus like CIBIL now place immense weight on how much of your limit you actually touch. Data from late 2025 indicates that individuals who maintain a CUR of under 30% see an average credit score increase of 45 points over twelve months compared to those who hover around 70%.

If your limit is 10 Lakhs, your sweet spot for spending is 3 Lakhs. This is not just a suggestion; it is a mathematical signal to lenders that you are not "credit hungry."

For an entrepreneur looking to secure a large-scale manufacturing loan or a mortgage in the future, this discipline is the foundation of your institutional trust.

Balancing Luxury Lifestyle and Fiscal Logic

In the world of premium metal cards and invite-only tiers like the Centurion or the high-end HDFC variants, it is easy to get seduced by the lifestyle perks.

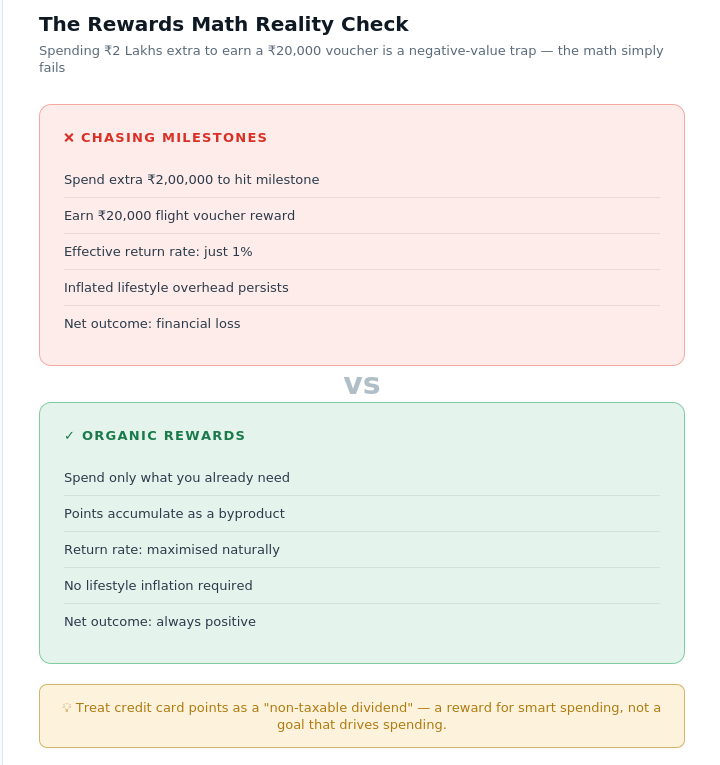

We see Indian professionals spending significantly on "milestone" goals to unlock travel vouchers or luxury stays. While these rewards are lucrative, they only make sense if the spending is organic.

If you are spending an extra 2 Lakhs just to get a 20,000 INR flight voucher, the math simply fails. A responsible user treats rewards as a byproduct of necessary spending, not a goal to be chased.

In 2026, the most successful wealth managers in Delhi and Mumbai are advising clients to treat credit card points as a "non-taxable dividend" rather than a reason to inflate their lifestyle.

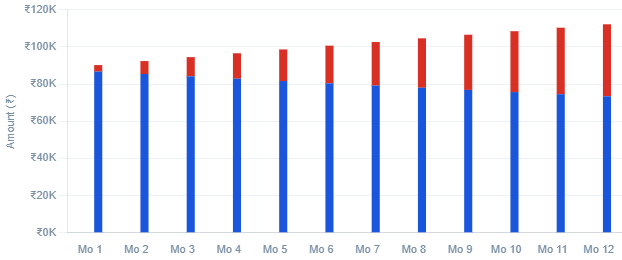

Visualizing the Impact of Compound Interest Traps

To understand why paying only the "Minimum Amount Due" is a catastrophic mistake, one must visualize the debt trap.

In the Indian context, where the monthly interest on cards can hover around 3.5%, the debt does not just grow; it explodes. Imagine a scenario where a professional carries a balance of 1 Lakh INR.

Graph Visualization: The Debt Spiral

Imagine a bar chart comparing two users. User A pays the full balance every month, and their debt remains at zero.

User B pays only the 5% minimum. Over 12 months, User B’s bar does not decrease significantly; instead, the interest component grows vertically, eventually surpassing the original principal if no further payments are made.

This "interest on interest" is what fuels the profitability of banks while draining the net worth of the elite.

By looking at the trajectory of such a debt, it becomes clear that the "Minimum Amount Due" is a psychological anchor designed to keep you in a cycle of perpetual payment.

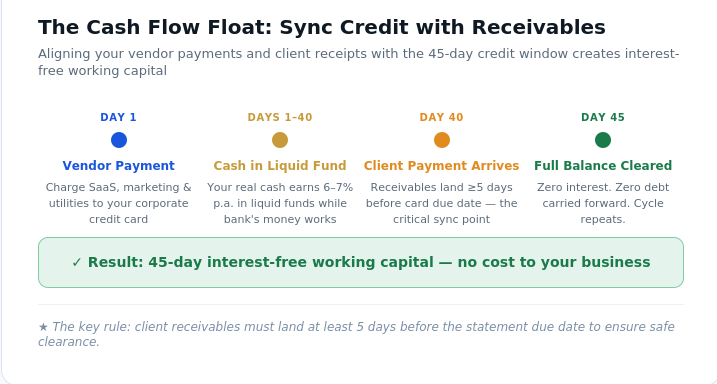

Leveraging Credit for Business Agility and Float

For a startup founder or an MSME owner, credit cards can be a strategic tool for managing "The Float."

This is the period between paying a vendor and receiving payment from a client. By placing recurring SaaS subscriptions, digital marketing spends, or office utilities on a high-reward corporate card, you effectively gain a short-term, interest-free loan.

The key here is the "Cash Flow Match." You must ensure that your client receivables land in your account at least five days before the credit card statement date.

This synchronization allows you to keep your actual cash in high-yield savings accounts or liquid funds for longer, earning a small but consistent spread on money that technically belongs to the bank.

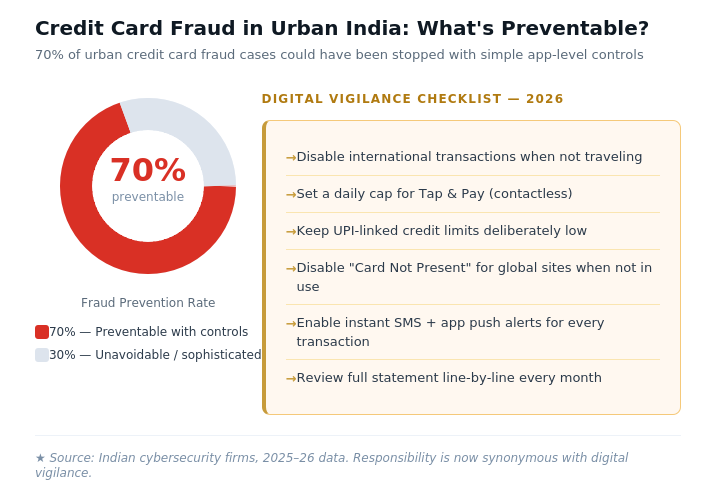

Shielding Your Wealth from Modern Cyber Threats

As we move deeper into 2026, the sophistication of financial fraud in India has scaled alongside our digital growth. Responsible use now includes a heavy dose of technical hygiene.

The "Set and Forget" mentality is dangerous. Every Indian cardholder should be utilizing the granular controls provided by banking apps.

This means disabling international transactions when not traveling, setting a daily limit for "Tap and Pay" transactions, and strictly keeping UPI-linked credit limits low.

Statistics from cybersecurity firms highlight that 70% of credit card frauds in urban India could have been prevented if the user had simply disabled "Card Not Present" transactions for global websites when not in use. Responsibility is now synonymous with digital vigilance.

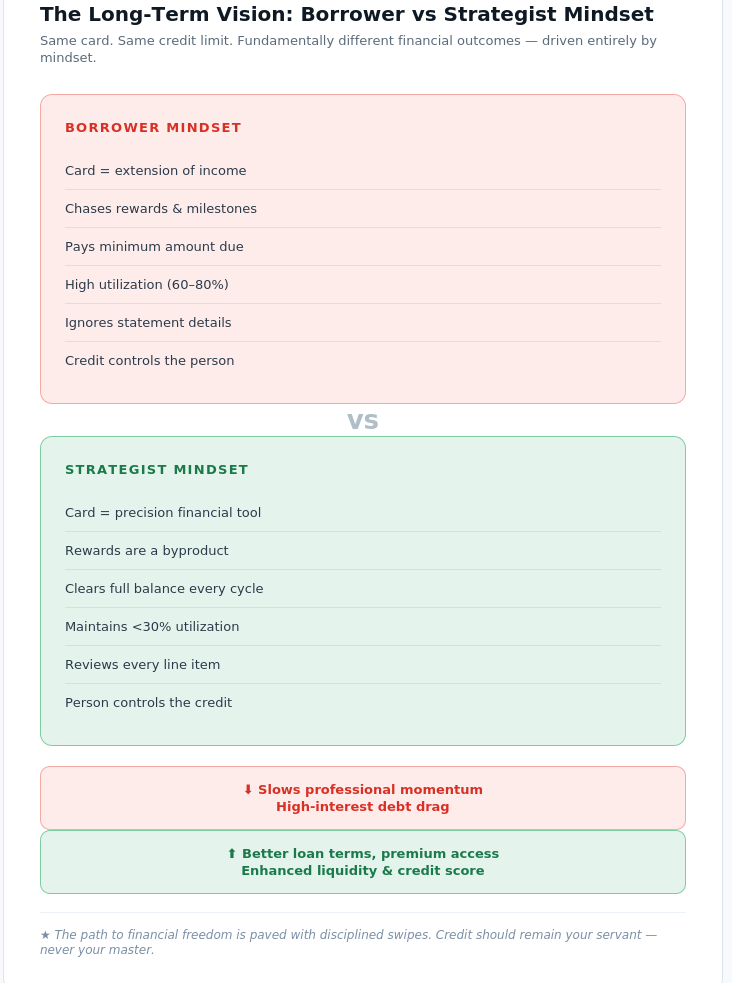

The Long-Term Vision of Credit Health

Ultimately, your relationship with credit cards in 2026 is a reflection of your overall mastery over your financial life. It is about moving away from the "Borrower" mindset and into the "Strategist" mindset.

When you treat your credit card as a high-precision tool, it rewards you with better loan terms, premium lifestyle access, and enhanced liquidity. When treated as an extension of your income, it becomes a weight that slows your professional momentum.

The path to financial freedom in India’s fast-evolving economy is paved with disciplined swipes and a deep respect for the power of leverage.

By maintaining low utilization, paying in full, and staying vigilant against fraud, you ensure that credit remains your servant, never your master.

- Business Finance

- Financial Freedom

Rahul Malodia is a leading business coach in India, a Chartered Accountant, and the creator of the transformational Vyapari to CEO (V2C) program. With a mission to empower MSMEs, he has trained over 5,00,000+ entrepreneurs to systemize operations, manage working capital, and scale their businesses profitably.

Known for transforming traditional business owners into confident CEOs, Rahul delivers India’s top business coaching programs through bootcamps, workshops, and online courses. His practical strategies and deep industry insights have made him a trusted name among entrepreneurs seeking sustainable and scalable growth.